Liquidity crises to persist and credit to private sector to continue falling in Zimbabwe

Bank deposits to GDP

One key indicator of financial sector development is ratio of bank deposits to GDP (BD/GDP). This is the total value of demand, time and saving deposits at domestic deposit money banks as a share of GDP. This measure determines the extent of banking in an economy and confidence in the financial sector. The introduction of the bond note will result in falling of BD/GDP at least by 30%. The ratio of all checking, savings and time deposits in banks and to economic activity and is a stock indicator of deposit resources available to the financial sector for its lending activities (Beck, Demirgüç-Kunt and Levine 2009). Banks need to attract deposits before they can lend. In Zimbabwe the economic impact of bond notes is that it is going to reduce the amount available for lending in the banking sector to the private sector. The attraction of deposits and savings in Zimbabwe or any country can only be a result high confidence in the banking sectors. Currency outside banking system to base money is the share of base money that is not held as bank deposits. In Zimbabwe a significant amount of not less than US$3billion is estimated to be circulating outside the banking sector. The level and change in currency outside the banking sector are frequently used as an estimate of the underdevelopment of the formal financial system (Schneider and Enste 2000).

Bank credit to bank deposits

The bank credit-to-bank deposit ratio (BC/BD) is a commonly used statistic for assessing a bank's liquidity by dividing the bank's total loans by its total deposits. BC/BD measures the financial resources provided to the private sector by domestic money banks as a share of total deposits. Domestic money banks comprise commercial banks and other financial institutions that accept transferable deposits, such as demand deposits. Total deposits include demand, time and saving deposits in deposit money banks. The news of the bond notes introduction has led to a severe depletion of bank deposits as people are withdrawing their US dollars and preferring not to bank them again. The economic impact as will be indicated by BC/BD will mean the current liquidity crises in the banking sector will worsen. Banks issue loans based on the amount of deposits they have, with loss in confidence in the banking sector there will be very low funds available for lending. The decline in lending will slow credit to the private sector resulting in slow economic growth which makes it unrealistic to achieve the target US$ 6billion exports targeted by RBZ.

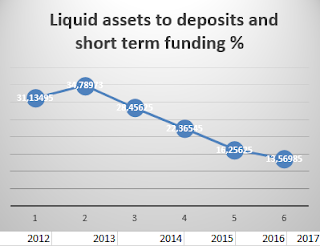

The ratio of the value of liquid assets (easily converted to cash) to short-term funding plus total deposits. Liquid assets include cash, trading, loans and advances, and cash collaterals. Deposits and short term funding includes total customer deposits (current, savings and term deposits) and short term borrowing (money market instruments). The figure has been falling since 2013 as per world bank figures available on the Global Financial Sector Development database, the 2015 figure is an estimate whilst 2016 and 2017 figures are projections which l made in the graph above. The projection above is merely to predict the worsening of the current liquidity crises which will not be solved by the introduction of the bond currency.

One key indicator of financial sector development is ratio of bank deposits to GDP (BD/GDP). This is the total value of demand, time and saving deposits at domestic deposit money banks as a share of GDP. This measure determines the extent of banking in an economy and confidence in the financial sector. The introduction of the bond note will result in falling of BD/GDP at least by 30%. The ratio of all checking, savings and time deposits in banks and to economic activity and is a stock indicator of deposit resources available to the financial sector for its lending activities (Beck, Demirgüç-Kunt and Levine 2009). Banks need to attract deposits before they can lend. In Zimbabwe the economic impact of bond notes is that it is going to reduce the amount available for lending in the banking sector to the private sector. The attraction of deposits and savings in Zimbabwe or any country can only be a result high confidence in the banking sectors. Currency outside banking system to base money is the share of base money that is not held as bank deposits. In Zimbabwe a significant amount of not less than US$3billion is estimated to be circulating outside the banking sector. The level and change in currency outside the banking sector are frequently used as an estimate of the underdevelopment of the formal financial system (Schneider and Enste 2000).

Bank credit to bank deposits

The bank credit-to-bank deposit ratio (BC/BD) is a commonly used statistic for assessing a bank's liquidity by dividing the bank's total loans by its total deposits. BC/BD measures the financial resources provided to the private sector by domestic money banks as a share of total deposits. Domestic money banks comprise commercial banks and other financial institutions that accept transferable deposits, such as demand deposits. Total deposits include demand, time and saving deposits in deposit money banks. The news of the bond notes introduction has led to a severe depletion of bank deposits as people are withdrawing their US dollars and preferring not to bank them again. The economic impact as will be indicated by BC/BD will mean the current liquidity crises in the banking sector will worsen. Banks issue loans based on the amount of deposits they have, with loss in confidence in the banking sector there will be very low funds available for lending. The decline in lending will slow credit to the private sector resulting in slow economic growth which makes it unrealistic to achieve the target US$ 6billion exports targeted by RBZ.

The ratio of the value of liquid assets (easily converted to cash) to short-term funding plus total deposits. Liquid assets include cash, trading, loans and advances, and cash collaterals. Deposits and short term funding includes total customer deposits (current, savings and term deposits) and short term borrowing (money market instruments). The figure has been falling since 2013 as per world bank figures available on the Global Financial Sector Development database, the 2015 figure is an estimate whilst 2016 and 2017 figures are projections which l made in the graph above. The projection above is merely to predict the worsening of the current liquidity crises which will not be solved by the introduction of the bond currency.

Comments

Post a Comment