Budget deficits, government debt and fiscal sustainability in South Africa

Whether

the federal government’s budget is fiscally sustainable or not is generally

measured by the annual in the ratio of debt held by the public to GDP (Levit

2011). This is known as the debt-to-GDP ratio. Budget deficits

will generally increase the level of total government debt. Temporary increases

in the debt-to-GDP are not necessarily problematic. However, if the debt to GDP

ratio is persistently rising, it is considered unsustainable. If GDP growth

equals or exceeds the annual budget deficits as a percentage of GDP, meaning

that the debt to GDP ratio would generally remain constant or fall, then the

budget is considered sustainable. While there is no level of debt to GDP that

is universally regarded as optimal, some budget reform proposals recommended

maintaining the debt to GDP ratio at 60% or less going forward.

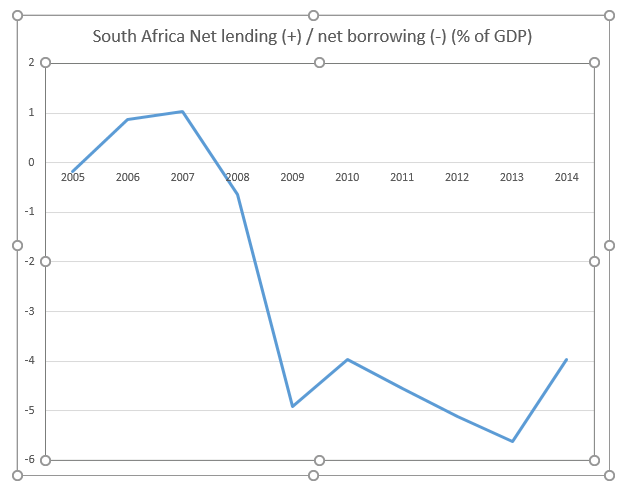

Net

Lending (+) and net borrowing (-) (% of GDP)

South Africa’s net lending as a percentage of GDP was

almost one between 2006 and 2007. It then fell sharply from 2008 to 2014. It actually

became a deficit of around -6%. This shows that the deficit ballooned over the

period. This sharp decline in net lending was brought about by the 2008/2009

global financial crisis. However, it continued to decline even way after the

financial crisis. This is shown in the figure below:

Debt

service on external debt

Over the period 2006 to 2016, South Africa’s debt

service costs generally rose with the peak being reached between 2012 and 2013.

Algeria’s servicing costs fell to almost zero between 2006 and 2007 and have

remained at that level for the whole period. Nigeria and Egypt also had very

low and stable debt servicing costs. This is despite the fact that Egypt was

going through a revolution. Overally, South Africa’s debt servicing costs are

higher than that of its counterparts. This is shown in the figure below:

GDP

Growth Rate

Since GDP is the yardstick that is

normally used to ascertain the economic growth trajectory of an economy, there

is need to look at the GDP growth rate of South Africa and that of its

counterparts. Only Algeria had a positive GDP growth rate over the period which

rose from slightly below 2% to almost 4%. South Africa’s GDP growth rate fell

from about 8% in 2006 to slightly above 2% in 2015. This also shows that the

growing budget deficit is consistent with a falling GDP. This is shown in the

figure below:

Inflation

Since

economists who hold the Ricardian view insists that budget deficits are linked

to a rise in inflation as the government may need to print more money to fund

the deficit, there is need to also analyse inflation rates. Nigeria had the

most fluctuations in inflation. The inflation rates for South Africa actually

fell during the period. In this case there is no evidence to suggest a causal

link between the country’s budget deficit and inflation. The findings are shown

in the following table and graph:

Inflation,

GDP deflator (annual %)

2006

|

2007

|

2008

|

2009

|

2010

|

2011

|

2012

|

2013

|

2014

|

2015

|

|

South Africa

|

6.2741538

|

8.8492898

|

8.8315689

|

7.5045113

|

6.3510265

|

6.532211

|

5.2866962

|

6.5876164

|

5.7012726

|

3.9568974

|

Nigeria

|

17.337782

|

4.7707422

|

10.835298

|

-4.3205733

|

103.8228

|

9.5100963

|

9.2712447

|

5.8732956

|

4.6626237

|

2.8636644

|

Algeria

|

10.546696

|

6.3953443

|

15.310571

|

-11.161609

|

16.119976

|

18.228012

|

7.4523735

|

-0.1122779

|

-0.4120846

|

-6.024195

|

Egypt,Arab Rep.

|

7.3608596

|

12.595542

|

12.208417

|

11.172961

|

10.115357

|

11.605866

|

18.228899

|

9.0038427

|

11.512876

|

10.940663

|

Debt

to GDP ratio

South Africa’s debt to GDP ratio

rose from 23.3% in 2007/2008 to almost 50% in 2016. The debt growth is

worrisome as this may make it unsustainable for the government as it has to

meet rising debt servicing costs. But since some economists argue that a debt

to GDP ratio of 60% or less is regarded as optimal, there may be no need to

worry if the government maintains it at a level below 60%. The data is shown in

the table below:

South Africa’s real GDP growth has

been falling since 2007/08 from 4.6% to 2% in 2014 whilst the debt as

percentage of GDP has been increasing from 23.3% in 2007/08 to 39.7% in 2013/14

fiscal year. The trend is government debt has been increasing due to deficits

whilst economic growth has been falling.

Conclusions

The running of a budget deficit by South Africa during

the 2008 global financial crisis was justifiable. It is reasonable to allow a

budget deficit during a temporary downturn in economic activity. During that

period the South African economy was negatively affected and the government had

to increase its spending in order to stimulate aggregate demand.

It can be concluded that South Africa’s persistently

rising budget deficits may raise a red flag to investors of an existing or

pending ‘fiscal crisis’. If South Africa continues to fund its budget deficit

with debt stock which surpasses the growth in output and income, investors will

then require to be paid a higher rate of interest. They will need compensation

to counter the risk that they might not be paid or that the value of their

securities would be eroded by inflation (which has risen from 4.82% in 2006 to

7.07% in 2016). Other countries experiences, like Zimbabwe for instance as

highlighted by Makochekanwa (2008), suggest that a loss of investor confidence

can arise abruptly during periods of budget deficits or uncertainty.

South African budget deficits are not going to be sustainable

in the long run because of the nature of the expenditure such as social

services which account for R884 billion which is almost half of the total

budget. A high percentage of the budget should go towards investment such as

agriculture, mining etc. and not financing state enterprises that are loss

making.

Comments

Post a Comment